In the past decade, Chinese companies have become more active in foreign direct investment (FDI) activities, not only for oversea natural resources, but also in search for new market space and technologies. However, what has been growing simultaneously is a fear, sometimes unreasonable, towards them from some of their target countries.

Read this article in Chinese

Macro landscape

Several decades after the adoption of the reform and open door policy, Chinese enterprises started to experience foreign direct investment (FDI). Started from Hong Kong, Macau and Taiwan, Chinese investors have marched into the United States, the United Kingdom, France, Germany, India, South Korea, Japan, Africa and Latin America. The first type of FDI was devoted to gain access to natural resources. But, more recently a second type of FDI has emerged: gaining access to new markets and technologies. For example, Huawei recently opened a top level Mathematical and Algorithmic Sciences Lab in France; Fosun Group, from Shanghai, acquired a French corporation called Club Méditerranée. Both are of this sort.

It is interesting to look at the timeline of how China invested overseas and received investment from abroad (Chart 1). From 1978 – when Deng Xiaoping first put in place the reform and open door policy to 1990, only few foreign firms were bold enough to advance into this new market. After 1990, China saw a spike in foreign direct investment mainly from the U.K., France, Germany and the U.S.A. among others. As of now, China received an FDI worth 100 billion dollars each year on average.

Chart 1: Inward & Outward FDI (1980-2006)

Source: CNUCED, http://www.unctad.org

There’s even one more important thing to look at: China’s outbound investment (Chart 2). In 2000, China invested a merely 7 billion dollars overseas. It was quite ridiculous considering the size of the country. Whereas from 2004 – the starting point when China’s outbound investment picked up – real changes took place as the Chinese enterprises were finally confident to go global. The revolutionary change of China was making more investment overseas than receiving it was an important landmark that opened a new chapter for China.

Chart 2: Chinese Outward FDI (2000-2012)

Source: MOFCOM

In recent years, we often saw global media headlines about acquisitions of international companies by Chinese ones: Lenovo acquired IBM’s personal computer business (2005), Geely bought up Volvo (2010), Shuanghui paid to own American food brand Smithfield (2013). The sales of Smithfield cost Shuanghui a huge sum of 4.6 billion dollars. Last year, Anbang Insurance paid a whopping 2 billion dollars to buy the Waldorf Astoria, a marvelous historic building in New York City.

Not all M&As attempts from Chinese companies have a happy end. In fact, it is rather easy to find a failed case. China National Offshore Oil Corporation (CNOOC) failed to acquire Union Oil Company of California (Unocal Corporation) due to the resistance by the American CFIUS (2005). Huawei’s bid to acquire 3Com, a computer network company also hit the rock (2007).

France is an interesting country to start with. In France, the type of the companies and the price at which they were acquired varied greatly from each other. Château Bellefont-Belcier and Château LatourLaguens are among traditional and prestigious châteaux in France. They now both have Chinese owners. What’s interesting is that Chinese rich people only buy châteaux to treat their acquaintances as a friendly gesture, not for commercial use. They are usually small deals worth around 30 million to 50 million euros. Nevertheless, French are getting worried, “Our red wine is all bought by the Chinese!” What a ridiculous idea. There are over 7,000 châteaux in Bordeaux alone, with only 50 of them being acquired by Chinese. People who held such thought cannot see the wood for the trees. They have probably overlooked a deal between China Investment Corporation and Gaz de France Suez worth 2 billion euros when the former took a stake in the latter.

A rather well-known German M&A deal was between Weichai Power and Kion Group AG that worth 738 million euros. In 2013, Sany Heavy Industries spent 324 million euros on Putzmeister, a German manufacturer of concrete pumps. It is common to see Chinese companies investing even in Switzerland, a European country only slightly larger in terms of population than the Pudong New District in Shanghai.

Chart 3: Acquisitions of international companies by Chinese companies , 2005-2014

How Scary Are Chinese Enterprises?

Considering the profile of the M&A deals mentioned above, it is fair to say that Chinese firms firstly took small steps when going global. After a while, they set their targets on large corporations and swiftly moved to other European countries.

In 2012, Chinese investment in the European Union only took up 2.6% of the overall foreign direct investment received in the region. Today, China contributed 15% to the global economic growth. That is why we should not rule out the possibility that China’s corporate investment will account for 15% of the entire foreign direct investment into the European Union. Obviously, Chinese enterprises’ foreign expansion just took off. There will be more frequent investment and M&A deals coming up.

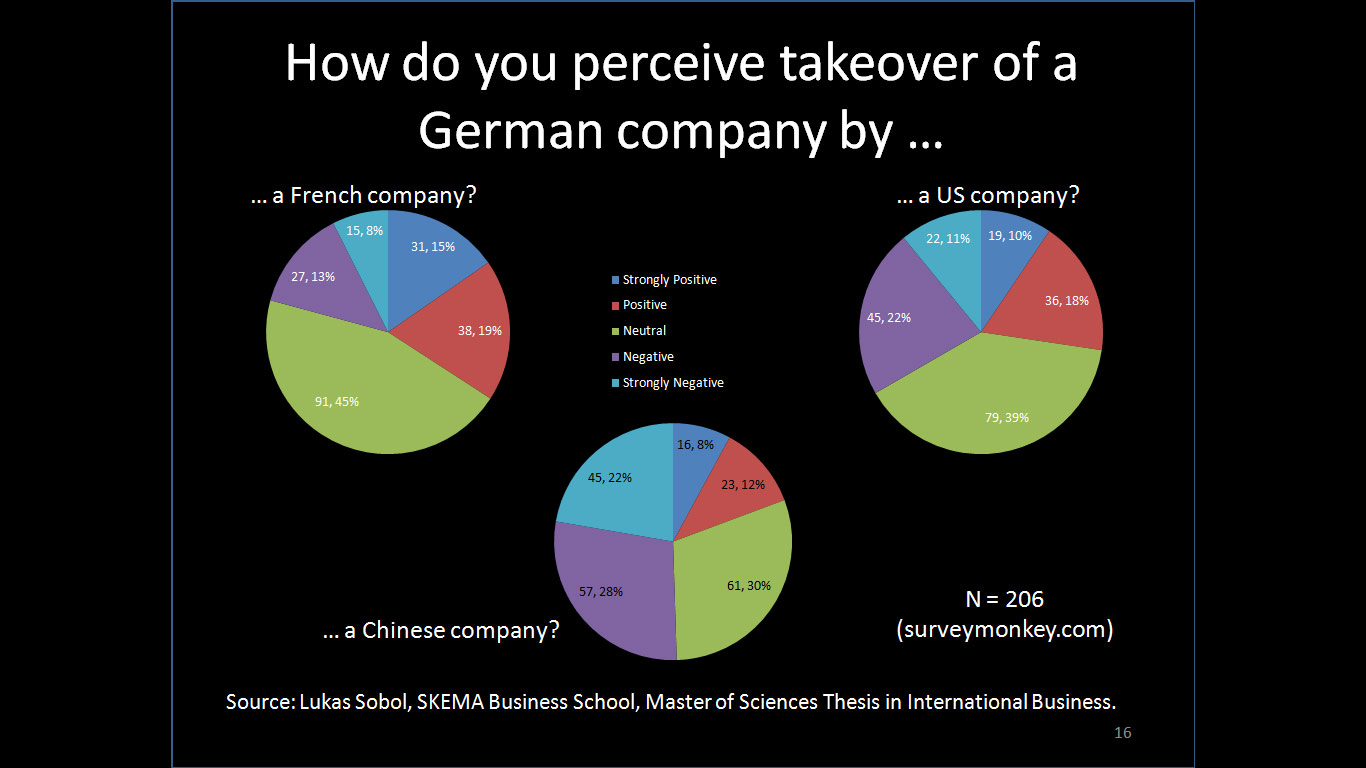

The problem is, shall Chinese be feared by us (foreigners)? We conducted a poll among Germans. “How do you perceive takeover of a German company by …?” The results showed that over 15 percent of those who were surveyed chose “strongly positive” if it was a French company. 10 percent said they would also strongly support a “U.S. company”, while only 8 percent expressed their strong favor of a Chinese company.

Chart 4: How do you perceive takeover of a German company by …

Source: Lukas Sobol, SKEMA Business School, Master of Sciences Thesis in International Business.

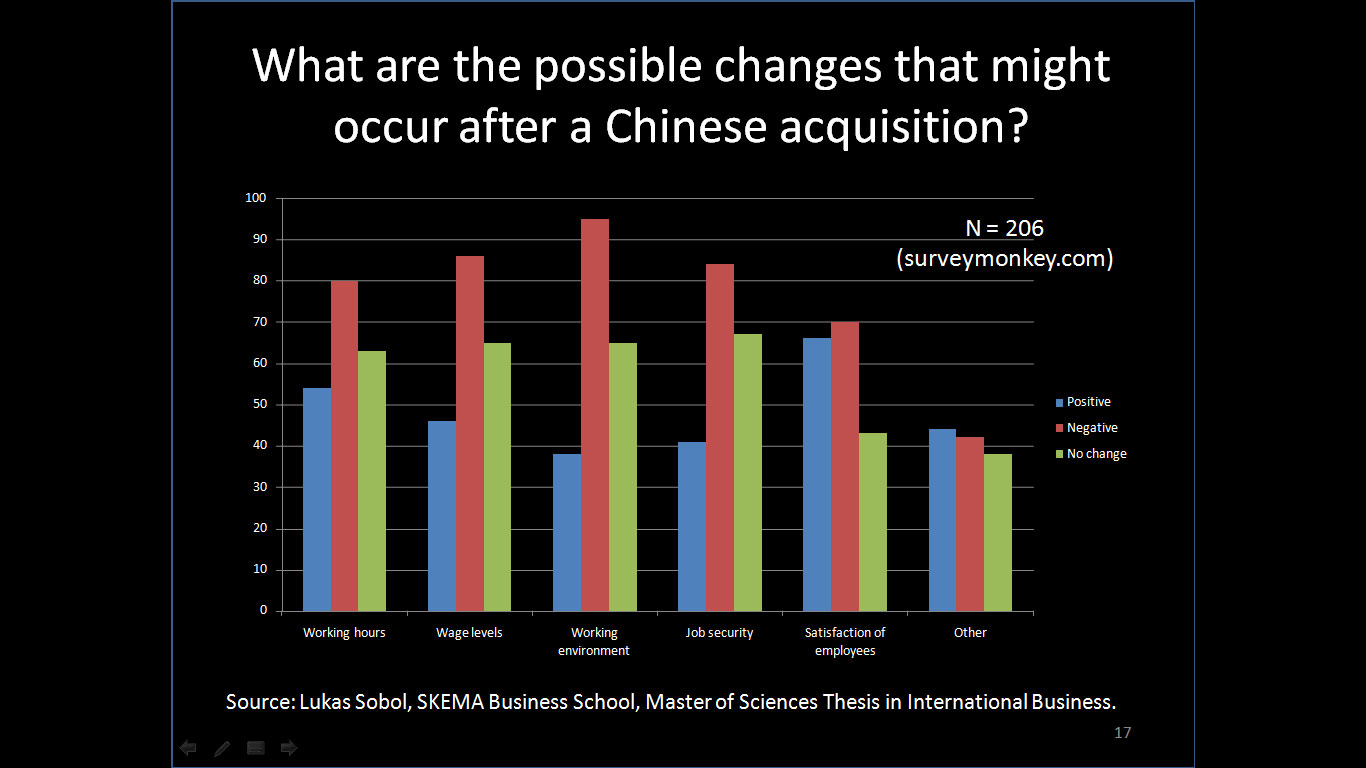

On the choice of “strongly negative”, only 8 percent of Germans voted so if it was for a deal with French. 11 percent held the same view against U.S. companies, while that number for Chinese companies was 22 percent. Germans are actually feared of Chinese, as the poll suggested. When we went deeper and asked German one more questions of “what could be possible changes that might occur after a Chinese acquisition”, we received appalling answers. They believed that their working hours, wage levels, working environment would all be negatively affected if their companies acquired by Chinese. Germans almost labeled all Chinese companies as demons who would imprison them as working slaves. They shattered that their “employment safety” would be deprived.

Chart 5: What are the possible changes that might occur after a Chinese acquisition?

Source: Lukas Sobol, SKEMA Business School, Master of Sciences Thesis in International Business.

With all being said, is it necessary for them to feel the fear? I believe the answer is no. In fact, foreign direct investment brings in a great deal of benefits to the local market. Acquisition deal means more cash and investment. On top of that, it introduces company products into the Chinese market. And furthermore, it gives rise to “scale effect” or “symbiotic effect”.

From a more macro perspective, a functional Chinese direct investment will produce more employment as well as interests spillover in other domestic companies. As for the vertical industry chain, procurement at both upstream and downstream is likely to grow and lead to more profits to suppliers and buyers. If we look horizontally, more active talents will be available as a result of more competition. Domestic firms can acquire new skills and cultural insights from Chinese companies. Workers dispatched to China will also gain a better understanding of the Chinese market for more engagement. These global-minded talents with overseas working experience are hot catches to enterprise. The economy can stay lively through this way of exchange, which has been proved to be of vital importance.

Hence, we should not be daunted by foreign acquisition deals. Instead, it is encouraged to invite more Chinese companies to France and provide them with means to clean negative sentiments against Chinese companies.

Two types of outward FDI

We can categorize Chinese companies going global into two management types. The first type is “resource seeker” from my perspective. China’s massive scale manufacture industry needs to be sustained by continuous input of energy and ore(iron, bronze, etc.). But China is not a country rich of these resources. As a result, countries and regions like Australia, Africa, South America and Canada where abundant natural resources can be found are popular investment destinations for Chinese companies. In fact, most of the investors are big state-owned enterprises and the deals largely reflects the State strategies. The most outstanding feature of the deal is trading with huge amount of cash for a decades-long contract. A mine usually has a life lasting as long as 20 years. The profit comes with a huge-volume contract is quite considerable.

The second type is “market or technology seeker”. In nature it can be understood as a business expansion in a horizontal way – Chinese companies running the same businesses only in a different country. As of now, most of the acquisition deals we see are between private and small companies, which are of clear difference from the first type. A typical case would be Geely’s acquisition of Volvo. Li Shufu, the chairman of Geely once said, “After we acquired Volvo, we would suggest the government not to buy Audi cars anymore. Instead, they should opt for Volvo, which is now a brand Chinese-own.” His statement represented both the business target of both Geely and Volvo: win over a larger piece of the Chinese market. Volvo opened up two new factories for assembly and engines after this win-win deal.

Another example is when Sany Heavy Industry acquired Putzmeister from Germany. Sany Heavy Industry, based in Changsha (Hunan Province) employs 70,000 people with a tenth of them doing Research and Development work. Sany owns over 5,000 patents, which is rarely seen in a field that is not so technology intensive as the semi-conductor or the pharmaceutical industries, but more like automobile, construction, machinery and infrastructure, where technological content is rather medium. Sany boasts a great deal of innovation in these low-end industries and shifted their attention to advanced technology in German. The Putzmeister deal is the largest acquisition of a German company that employees 3,000 people by a Chinese firm. This was a rewarding deal to Putzmeister as well.

Shanghai Bright Food bought Weetabix, a British cereal producer, Tnuva, a diary company from Israel and Manassen from Australia. What’s the purpose behind its purchasing moves? Different rules apply to different commercial fields. Research and Development lies at the core of pharmaceutical industry, while brand is the top priority for food industry. One would pay most attention to brand and logo when doing groceries in the supermarket. Bright Food bought Weetabix for its reputation and its brand image, in hope for some presence in the British market. It is the same with purchasing Tnuva, which is the second diary company in Israel. Shuanghui and Smithfield mentioned above are also well-known brands in food industry.

What is worth mentioning about brand image is that Chinese people have low trust in local food brands. Companies in this area bought prestigious foreign companies in an attempt to reinvent the company image. Some even tried to get rid of the entire Chinese features to look anew.

Chinese companies are also buying to seek diversity in branding and marketing. The Sanpower Group recently acquired the House of Fraser from Britain. With a British brand under the Group, Sanpower established its presence in the U.K. and posed to tap into a new market.

To conclude, I would like to stress that it is getting harder for Chinese companies to go global and the reasons for this phenomenon. In France, the workers’ union would be a tough challenge. The union is such a powerful organization that it can call upon workers’ to go on strike if there’s ever a misstep made by the employer. Chinese companies have to deal with this fact if there were to invest in France. One must get himself familiarized with the 2.000-page long France Labor Law as well as the complicated tax rules. The most effective way is to hire a local consultant to save time. Another tough question is: who will be the head of the joint venture or the new company? Be cautious if it comes to a decision of replacing a French manager with a Chinese one, or appointing two managers with one from China and the other from France. This problem is much more complicated than expected. It is suggested to take into consideration of the industry and environment the company is in, and more importantly, human aspects.

Political solutions will also work. But we must move ahead and develop, which is the most important. There will be more Chinese enterprises springing up in the world stage. These Chinese companies must work together with local ones to create more, instead of less, opportunities for development. (Translated by Suwen Feng)

京公网安备 11010502032941号

京公网安备 11010502032941号{kind=link}